Now that Santa’s back home, trying to figure out how to get rid of his leftover inventory, with the new year well under way, it’s time for a reality check on what the retail landscape is going to look like for 2015 and beyond. What are some of the major issues and market characteristics that continue to evolve, and those that we are stuck with that are largely out of anyone’s control to change?

For starters, regardless of a few pockets of cheer, once again the retail industry has managed to stumble through another rather mediocre Holiday season. Once all of the insane promoting and discounting is factored in, as well as tallying up the excess inventory that will have to find a hole somewhere to bury itself, mediocre may turn into bleak and unprofitable.

On a more positive note, perhaps this will be the year in which we finally witness the serious elimination of excessive retail space, including malls and shopping centers, and the downsizing of what remains. I said perhaps. Part of the weeding out should consist of retailers who have reached the end of the line financially, due to their inability to steal business from competitors in a slow-to-no growth marketplace, (examples: Deb Shops and Delias). The other part of the shakeout should include retailers who are stuck in the last century (examples: Sears, Kmart and Radio Shack), unable to transform their strategies and business models necessary to engage the 21st century consumer, now the “controller in chief.”

Overcapacity Feeds on More Overcapacity

Note that I said perhaps the industry will shed excess capacity, followed by the likes of those who should be eliminated. And the reason for not holding my breath while I wait for this to happen is that I’ve been holding my breath for at least a quarter of a century. Year over year, the perhaps and should never turned into will and did. Worse, more net space just kept piling onto the excess.

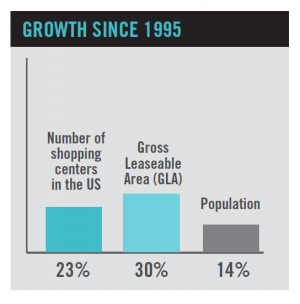

Since 1995, the number of shopping centers in the US grew by more than 23% and GLA (total gross leasable area) almost 30%, while the population grew less than 14%. Currently there is close to 25 square feet of space per capita (roughly 50 square feet if small shopping centers and independent retailers were added). In contrast, Europe has about 2.5 square feet per capita.

Although each year there are mall and store closings, the elimination of retail space, and now perhaps websites, is not occurring as rapidly as the emergence of new or replacement space entering the marketplace. The primary and underlying reason for this condition, and why it will continue ad infinitum, is that growth expectations/demands of shareholders, independent owners and Wall Street are higher than the growth of the real economy. And this has been the case for at least the last 25 years. So as businesses continue to adhere to this delusional reality, I offer a list of some of the more self-deluding tactical decisions that businesses make for quick (or any) growth. Self-deluding, because in the aggregate, these decisions simply lower all ships by exacerbating the ongoing and long-term increase of over-capacity.

- Every time a retailer opens a new door it’s an immediate new revenue stream for growth. So why not? Too many stores are somebody else’s problem.

- There are financial barriers to closing underperforming stores, not the least of which are penalties for breaking lease covenants.

- Realtors’ willingness to incentivize (cut deals) for retailers enables them to stay in business.

- As long as an underperforming door in a chain is “breathing,” it may be financially less costly to keep it open than to close it.

- Productivity of underperforming doors and/or space is not always easily or measurably identified.

- Many underperforming malls are repurposing or relocating as neighborhood, lifestyle shopping villages. This is not a bad idea. However, it simply moves the space to another area without reducing it.

- Outlet store shopping centers are growing at a rapid pace. And traditional full line retailers are opening more outlets than full line stores because they provide greater growth and profitability.

- Off-price retailers are rapidly expanding.

- Just as there is too much stuff sloshing around the globe, so too, there’s too much capital in pursuit of investing in even more capacity and/or propping up “losers” (iconic brands that investors believe can be fixed).Sort of like the Fed and “Government Motors,” (the bailout of General Motors), and of course, Sears et al.

- The liberal and strategic use (or misuse) of bankruptcy during which businesses shed debt, renegotiate contracts, and emerge as new low cost competitors, helps perpetuate overcapacity.

- The continuous stream of foreign brands and retailers entering the US marketplace, believing that “if you build it, they will come,” totally misunderstand the most congested and complex marketplace in the world.

- Finally, of course, the unrelenting acceleration of e-commerce, with virtually no barriers to entry, including financial, is building incomprehensible overcapacity. This is an unprecedented phenomenon and there are no measures that indicate these enormous additions to the supply side are being offset by corresponding declines in the brick-and-mortar and any other retail sector.

Share Wars Forever and Darth Vader’s Nasty Weapons

We are operating in an increasingly overstored, overstuffed, and over websited environment, in an economy in which consumers’ wallets are barely growing at best and shrinking at worst. Competitors must battle for enough of a share of this rather stagnant market (growing 2-3%), to grow their own businesses at a high single, or low double-digit rate. And they must do so profitably.

This growing conundrum of increasing overcapacity as bulleted above is now exploding with the fuel poured onto its fire with insane price promoting and discounting required to achieve such growth while still maintaining profitability. Let us count the ways:

- 70% is the new 40%

- Buy one, get several free

- Gift with purchase

- Couponing

- Loyalty programs

- Hundreds of new e-commerce “deals” popping up daily

- Opening more outlet stores than full-line stores (across all retail sectors)

- Diffusion and subbranding among the luxury and designer brands

- Price-changing, algorithmic software

- Price matching

- Showrooming

- Sharing

- Auctioning

- Swapping

- Renting

- Repurposing, selling used goods

- The daily onslaught of new e-commerce businesses, many of which do not make any profits as they tap into multiple rounds of funding, thus affording them the advantage of setting prices below costs to capture share of market

So discounting which used to be the tactical weapon of choice is now the strategic weapon of necessity. In this “race to the bottom,” where is the bottom? Is it when there are no more costs that can be cut, when margins are eroded to the point at which retailers are barely able to stay in business? And then does that rock-bottom price become the consumer’s new and much lower measure of the value of your brand or store? Indeed, the Darth Vader and share wars metaphor is an understatement.

Consumer Power, Shifts and Expectations

While tearing your hair out trying to figure out how to escape the sucking vortex depicted above, there are some major changes happening among consumers that add to the complexity of staying one step ahead. However, before reviewing those, there is one constant among all consumers today, which is intensified by the Internet and technology. Consumers wield the power of overabundance of choice, now on technological steroids. They have unlimited and instantaneous access to whatever their hearts desire, a key tap away, or in another store across the street. This adds even more fuel to the retail fire.

Here are five major strategic shifts evolving in the marketplace:

- Widening Income Gap

This gap is expected to continue and bodes well for luxury, discounters, off-pricers and outlet sectors. - Urban Migration

More than 80% of the population lives in cities and it’s growing. This drives small neighborhood store strategies like Walmart Express, City Target, Bloomingdale’s and many others, as well as the accelerating growth of neighborhood lifestyle shopping villages and small independent shops in urban areas. - Population Shift

Millennials will replace (and eventually become) the Boomers. The Next Gen is expected to account for 30-40% of all retail sales by 2020. Boomers are retiring and downsizing their lives, spending more on travel, leisure, entertainment, health and welfare than on stuff. Both of these shifts will drive big strategic and structural shifts. - Racial and Ethnic Diversification

In the US, the white population will shrink 23% by 2050; blacks will increase by 11%; Asians by 74%; and Hispanics by 57%. This demographic shift will drive huge strategic and structural changes. - Consumers Are the New POS

With every mall, store and brand in the world sitting comfortably in consumers’ pockets (smartphones), all businesses must now be digitally and physically accessible to each consumer whenever, wherever, how and how often they so desire, and only if they have granted you permission to enter their space.

How to Beat Darth Vader and the Share Wars Conundrum

Just as swimmers are advised to swim sideways when being sucked out to sea by a rip tide, move sideways out of the sucking vortex described above. Take a strategic pause, and go back to “101” basics. The consumer is in the center of the proverbial universe, reigning supremely omnipotent. As you may have known ever since these share wars started, all you have to do is be able to answer the following six questions — and then, of course, be able to implement them.

- What is the unique, sustainable experience that I am creating or co-creating with my target consumer?

Best product/brand/service, best price, and immediate access are just the price of entry today. - How is this experience being increasingly personalized for each unique consumer?

Big Data, technology and the Internet make this possible today. - Do I need to create consumer access to my brand, stores or website at multiple price points? If so, how?

Big Data and technology can determine consumer accepted different tiers of credible value. - How do I increase the flow and rapidity of new product and experiences into every point of distribution?

Technology can reduce cycle times and along with Big Data can drive lean inventory and a more rapid flow. And the integration and interchangeability of omnichannel can drive the right product and its quantity to the right place (distribution point), at the right time (when, where and how often the consumer wants it). - Do I understand and connect with every “community” that is important to my target consumers, both online and off? Does my brand, store, product or service understand and connect with the values of my consumers as well as their definition of the value of my offering? Big Data and technology facilitates this kind of connection and understanding.

- How can I utilize technology to create a better experience for the consumer both online and off?

This starts with technology driving speed, efficiencies and productivity in the back end of the value chain, Big Data, technology and omnichannel for the creation and precise, timely distribution into each distribution point, and finally the smartphone, apps, and technological devices to delight the consumer and elevate the experience at the POS, both online and off.

These are simple questions requiring awesome answers and implementation. But if you can nail these questions with precise and clear answers, understandable throughout your organization, and have the organizational horsepower to rollout those strategies across your enterprise, then you will be the Jedi Knight blasting Darth Vader into oblivion. And for you, at least, share wars will be over. And 2015 may be the beginning of us traveling back to the future.