A Brief History and Consumer Perspective

A Brief History and Consumer Perspective

Women’s underwear, its euphemistic pseudonym ‘intimate apparel,’ or its more sophisticated sister, ‘lingerie,’ is difficult in so many ways. For all of us women consumers, it is a necessity; a purchase that must be made and replenished regularly. And, trust me, as a consumer who has been buying her own underwear for more years than I’d like to count, it is not always an easy, satisfying, fun, or self validating purchase.

Underwear is a category of apparel that gets us down to the bare bones of ourselves. Our bodies. Our comfort. Our sense of self. Our sex appeal. Our underpinning. The foundation for all of our clothes. Women’s underwear has been marketed to us for generations reflecting deep-seated emotions and attitudes about ourselves, our roles, and our history as women. From long before the time women discarded their bras in the late 1960s as a symbol of second-wave feminism, bras have had a history of women’s emancipation and independence. In 1873, writer and activist, Elizabeth Stuart Phelps, wrote: “Burn up the corsets! … No, nor do you save the whalebones; you will never need whalebones again. Make a bonfire of the cruel steels that have lorded it over your thorax and abdomens for so many years and heave a sigh of relief, for your emancipation I assure you, from this moment has begun…”

Big Business

As a category, with sales estimated over $11 billion last year, and outpacing the growth of women’s apparel overall, women’s underwear is made up of several product segments: bras, panties, shapeware, sleepwear and daywear — which means mostly slips and camisoles. The most important product segment is bras representing up to 50% of category volume. And, let’s face it, the reason bras are so important is that they support our breasts, that great symbol of womanhood, whether by making them bigger with padding; giving them a lift with an underwire; changing their shape; maximizing; minimizing; separating; pushing them up; or holding them in place for sports. Bras have both a real and invented performance criteria. They must fit and be comfortable enough to wear day in and night out. For many of us, bras require at least an initial try-on; which means at some time or another visiting a store, going into a poorly lit, generally ill- equipped fitting room, taking off our clothes, facing our bodies in the mirror, seeking assistance from sales people who are usually not available to help you when you are undressed, and trying multiple styles before finding one that does the job of whatever we want it to. I’m a person who likes, sometimes even loves to shop; the only category I can think of that is more difficult to shop for is bathing suits, and those we can put off buying for another season or do without entirely.

When I came of age, bras were sold by somewhat knowledgeable salespeople in independent specialty stores or department stores who stood behind a counter where the bras were stored and then handed selected styles to you to try on. Sometimes, the salesperson accompanied you into the dressing room to help you find the proper fit. Responding to women’s independence and to improve productivity on the sales floor, bras and panties became a ubiquitous sea of garments, hung on flimsy plastic hangers on T-bars in crowded, difficult-to-shop areas of department stores or, floating on wall racks in discount stores, with little differentiation except cumbersome descriptive tags conveying brand identity, product features and benefits — needed to replace sales experts. To this day, it is difficult, if not impossible, for any of us, without assistance, to sort through the styles we like to find the size that we think will fit us. I challenge any man to try it.

Retrospectives

The recent history of women’s intimate apparel is a story of industry consolidation, retail dominancy, and high-stakes marketing. In the past, leading brands including Bali, Warners, Olga, Maidenform and Vanity Fair competed for customer preference and loyalty with product innovation and advertising. Maidenform, founded in 1922, and family controlled until 1997, launched its famous “I Dreamed” campaign in 1949, which ran successfully for over 20 years. Women “dreamed” of fighting fires, going on safaris, joining circuses and opening the World Series outfitted in their bras. Somewhat revolutionary at the time, and, certainly distinctive, manufacturers like Maidenform depended on advertising to distinguish their products for consumers and retailers alike.

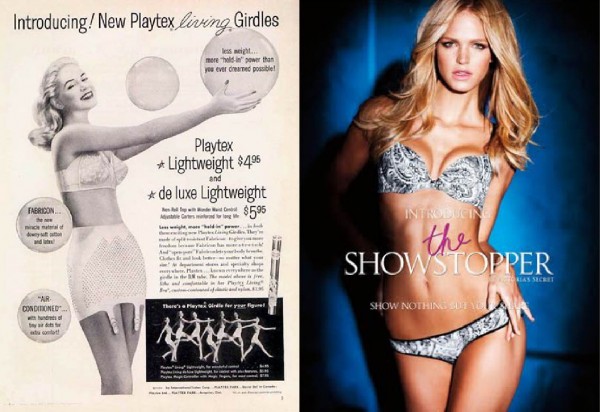

Playtex, an innovator in bras and girdles, owned 25% of the market share for bras by the early 1980s. Playtex featured size charts to facilitate shopping and named their products sensibly to reinforce product feature/benefits. Introduced in 1960, Playtex’s 18 Hour Bra signifies comfort to this day. In 1955, Playtex was the first company to advertise bras on television. Playtex launched its ‘Living Girdle’ in 1940. A latex girdle, which was actually rubber, replacing heavy boning and lacing, was considered an innovation because it allowed more comfort and freedom of movement, if not breathability. A 1949 ad for a Playtex Pink-Ice Girdle “with power stretch that slims you to the perfect lines of fashion’s new silhouette” shows that some things never change. But, the intimate apparel industry did.

“

In 1977, Ray Raymond launched Victoria’s Secret, “a store men could feel comfortable buying lingerie,” which grew into a somewhat successful catalogue business by 1982 when Les Wexner bought it for $4 million. Wexner positioned the brand as “tasteful sexiness,” maintaining the catalogue with a faux London headquarters while launching 346 stores between 1983 and 1990. By 1998 the company had a 14% industry market share. Today Victoria’s Secret has sales of $6.57 billion with 985 Victoria’s Secret and 34 Pink stores in the US with market share estimated at up to 40%. (For more on L Brands, see the Robin Report article by Marie Driscoll.)

What Victoria’s Secret did was revolutionary. Victoria’s Secret simplified the shopping experience, taking it away from those boring, difficult to shop department stores; capitalized on women’s attitudes about themselves and their bodies — focusing on sex appeal and sensuality, and, most important, made shopping for intimate apparel easy, special and fun. If Playtex was a prize marketer of yesteryear, Victoria’s Secret stole that prize in the 1990s and continues to market vigorously, aggressively and successfully today with its super models, sexy ads and live runway shows.

Consolidation

Today the industry is controlled by four companies: L Brands, Hanesbrands, Fruit of the Loom and Jockey. L Brands (Victoria’s Secret) dominates. Jockey, which introduced women’s underwear in 1982, has always been privately held. Hanesbrands, Inc., which “sells more units of intimate apparel, male underwear, socks hosiery and T shirts than any other company,” estimated sales of $5.1 billion for 2013, completed its acquisition of Maidenform for $583 million in October, 2013; its other brands include L’eggs, Hanes, Champion, Playtex, Bali, Wonderbra, Lilyette and Flexees. Fruit of the Loom, which also owns BVD, was acquired out of bankruptcy by Warren Buffet for Berkshire Hathaway in 2002 for a bargain $835 million in cash, purchased Vanity Fair Intimates in 2007 from VF Corp. Underwear is just the kind of predictable, commodity product Warren Buffet seems to like. And today most of these products are just basic commodities.

With the exception of Victoria’s Secret, now a mature business, and the introduction of SPANX which almost singlehandedly reinvigorated foundations, and is now a hot, leading brand, all that has really changed in the industry is the exchange of brands from one hand to another.

Changes in intimate apparel are reflective of overall apparel industry changes. The diminution of the department store as the leading channel of distribution; the proliferation and sameness of products; the inability of the industry to keep ahead of changing consumer attitudes; the failure of individual brands to market innovatively — or to make a profit, have all combined to form the consolidated intimate apparel industry we see today

A few boutique retailers have emerged that are designed and merchandised to help women enjoy buying intimate apparel. These upscale niche players including Journelle, Agent Provocateur, Bra Smythe, Intimacy and La Perla, provide a better shopping experience than department stores and more quality and elegance than Victoria’s Secret for those who can afford or aspire to afford it.

But relatively speaking, these brands are a microscopic niche and do not have enough critical mass to revive a stagnant, and what should be, exciting category where brands and retailers alike can profit and consumers can have fun.